WHEAT REJECTS TARGET. NEW CROP CORN ARGUMENT & MORE

MARKET UPDATE

You can scroll to read the usual update as well. As the written version is the exact same as the video.

Timestamps for video:

Overview: 0:00min

Corn: 2:05min

Beans: 8:05min

Wheat: 11:40min

Cattle: 14:40min

Want to talk about your situation?

(605)250-3863

Futures Prices Close

Overview

Soybeans were on the strong side today, while the rest of the grains complex saw some weakness.

Overall it was a pretty quiet day as for news, there wasn’t anything too noteworthy in the markets today.

The wheat market is running into resistance right at those golden zone targets we've been talking about.

Soybeans continue to chop sideways near the highs. Despite a wide 28 cent trading range for the last two weeks, every single close has been within 8 cents of each other.

Old crop corn has been weak to sideways, while new crop corn has actually performed well (which we will touch on later).

First notice day is this week, which can naturally add some pressure.

The next big set of data is going to be March planting intentions.

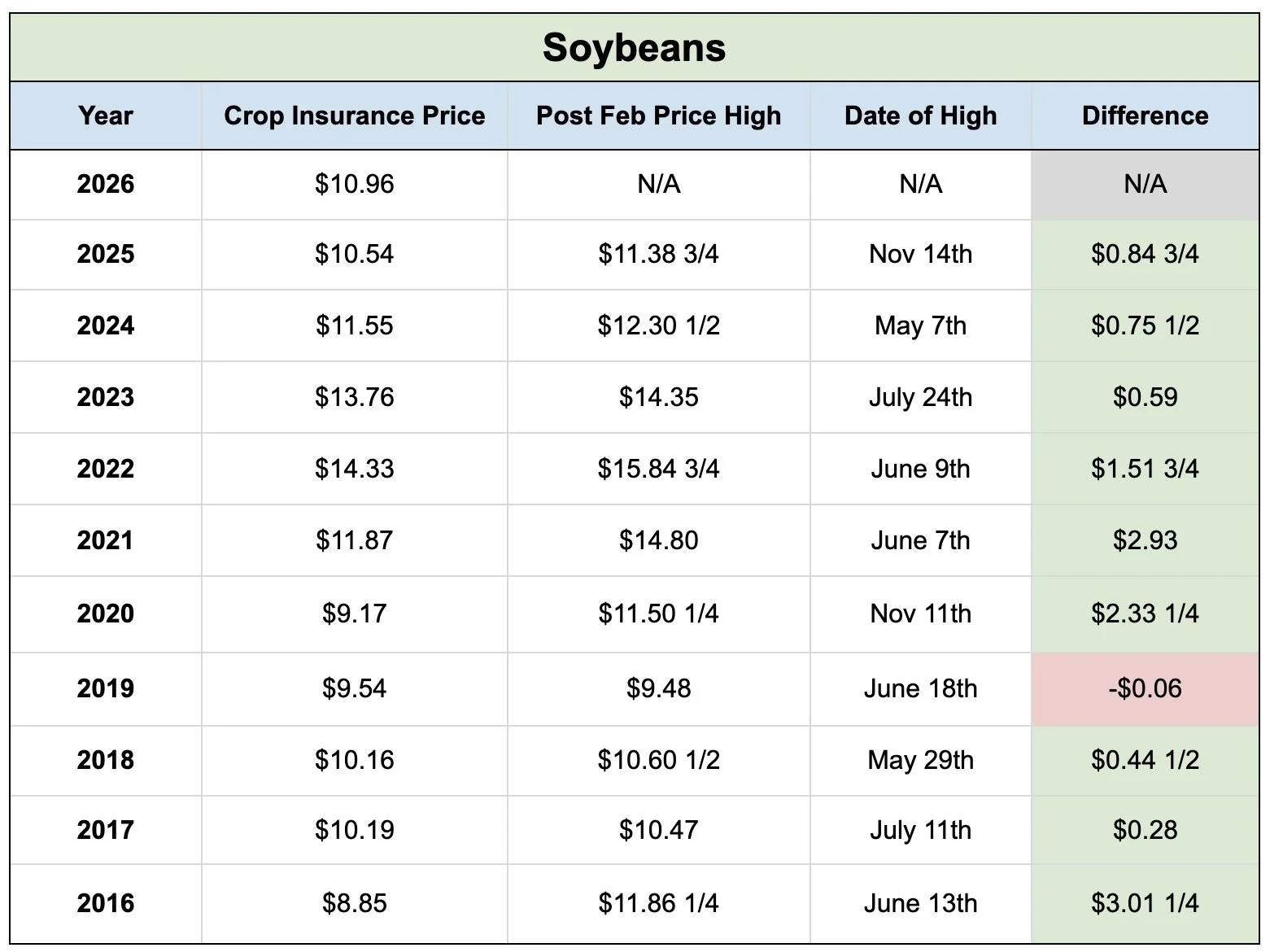

Insurance Average:

The current Feb price avg for new crop are:

Corn: $4.60 (vs $4.70 last year)

Beans: $11.04 (vs $10.54 last year)

Just a reminder, below is the data for crop insurance prices vs the highest price of the year.

More often than not, both corn and soybeans do tend to surpass that price at some point during the year.

The average move to the highs:

Corn: $0.65

Beans: $1.29

But keep in mind, the data is slightly skewed due to the bull market years in 2021 and 2022.

However, if you notice.. almost every high comes within that May to June timeframe. Which is why we like being more patient in new crop compared to old crop.

Seasonally, that is the window of opportunity.

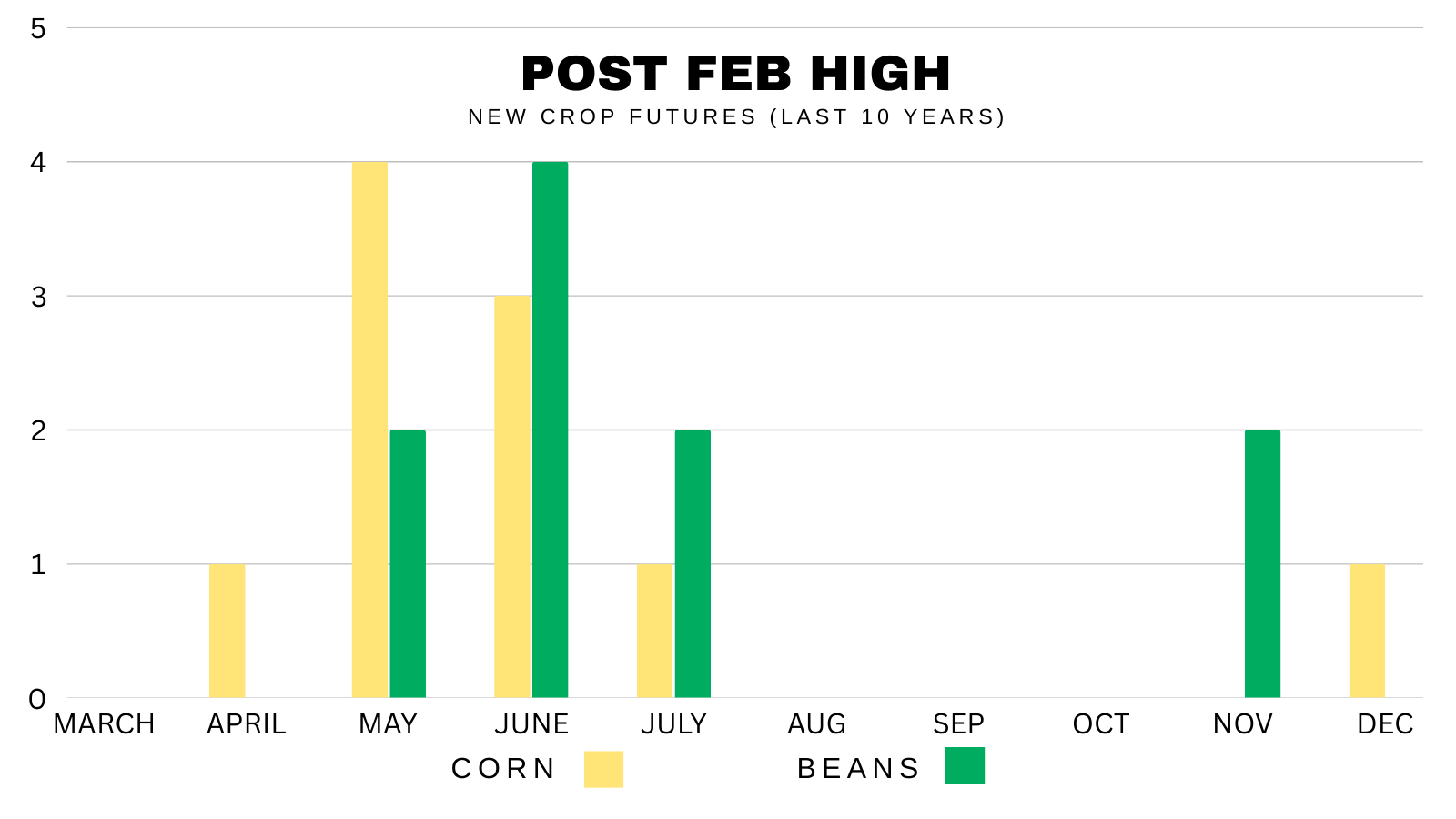

Post Feb High Data:

Here is the last 10 years of data from those tables above.

70% of the time, the corn high came in May or June.

80% of the time, the high came in May to July for both corn and soybeans.

Today's Main Takeaways

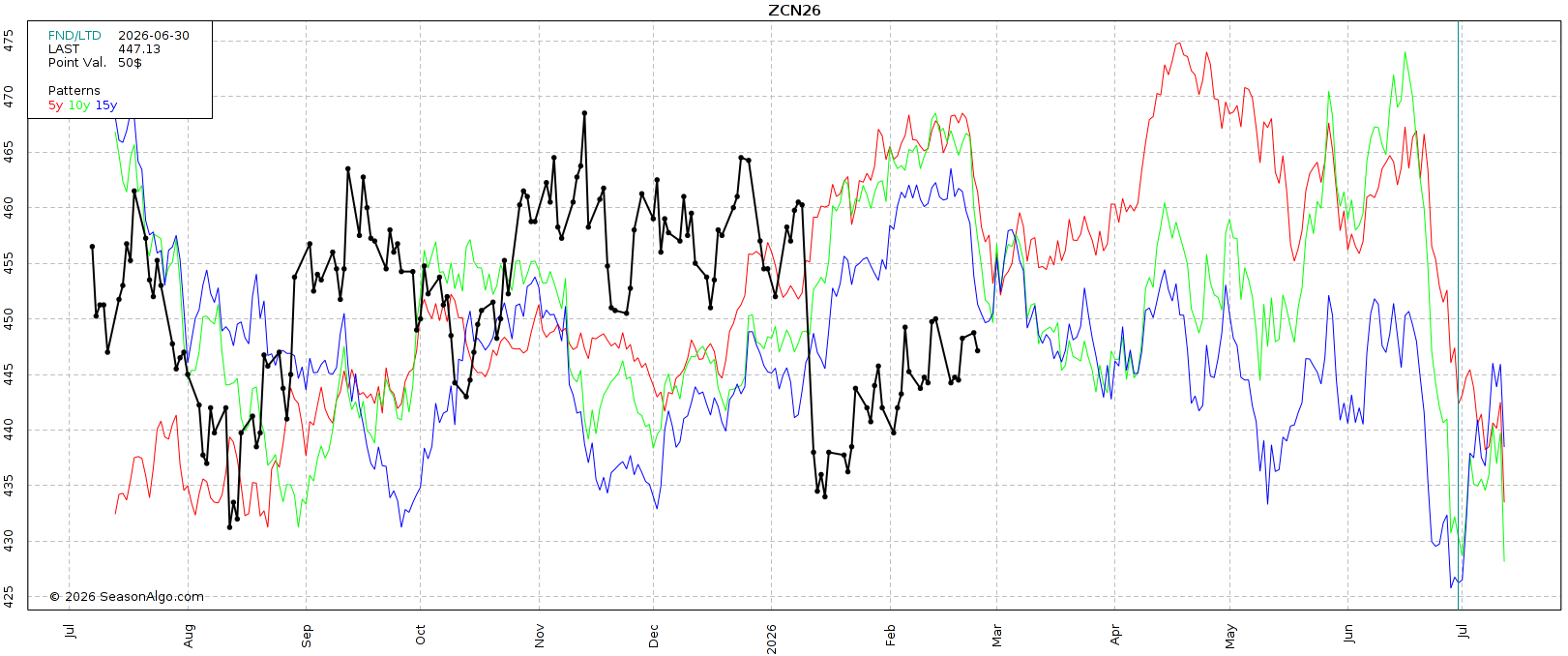

Corn

Fundamentals:

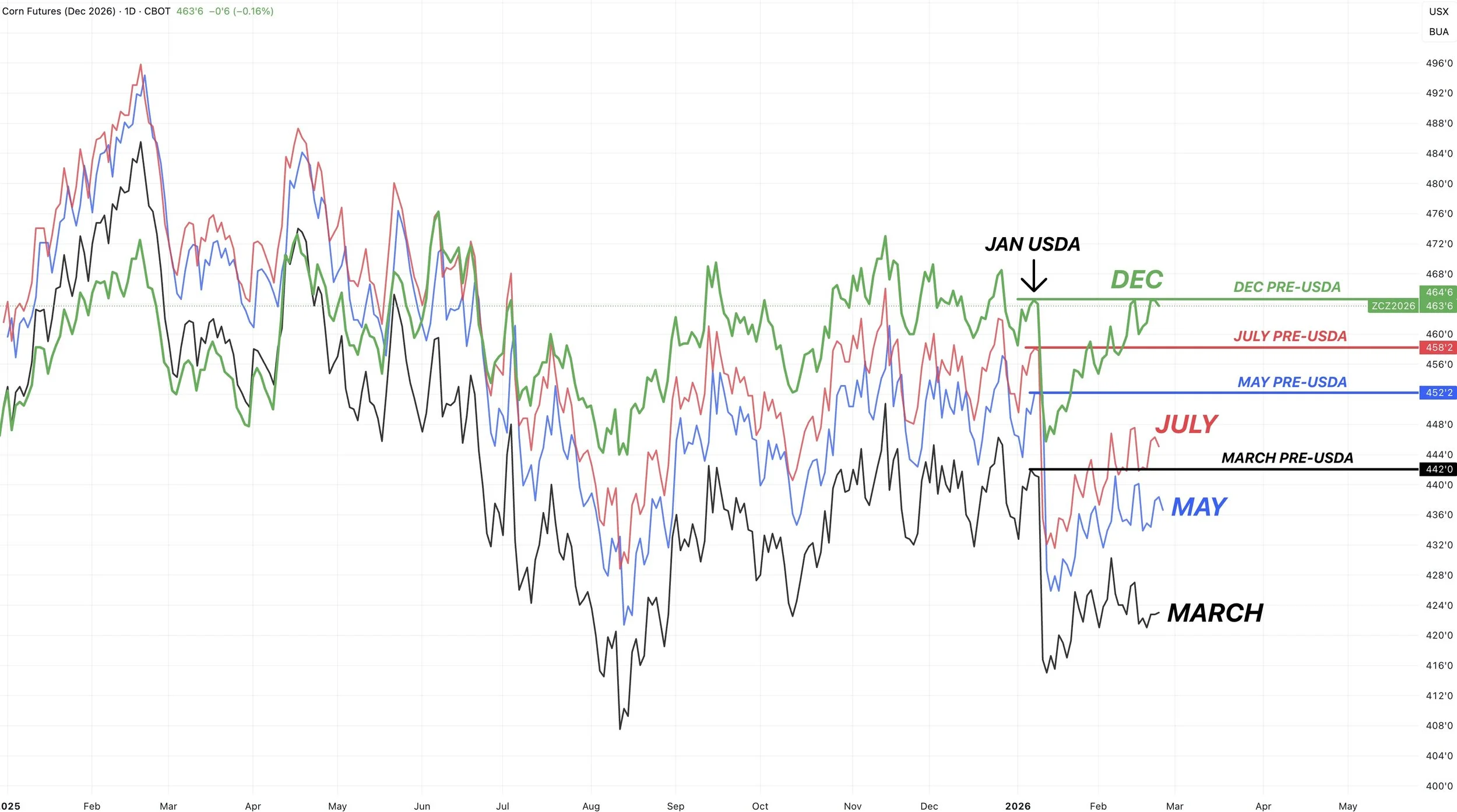

Corn has been weak in the March contract, but held up better the farther out the contracts go.

For reference, here is how much each contract has changed since before the Jan USDA report, where we sold off.

March: -18 cents

May: -15 cents

July: -12 cents

Dec: +1/2 cent

New crop corn is actually higher than we were before the Jan USDA report came out.

(Chart shows current prices vs pre-USDA prices)

Short term, first notice day this week is still a concern and has me cautious here.

Sometimes, we can even struggle for a little while after first notice day.

Here is the date we posted our first notice day lows the last 3 years:

2025: March 28th

2024: Feb 26th (weakness was front-run)

2023: March 10th

We do tend to carve out some seasonal lows here soon after first notice day.

In the 5-year seasonal the low comes early March.

In the 10 and 15-year seasonal the low comes at the end of March.

Both suggest higher by spring.

Supply vs Demand:

As I've stated for a long time. It's hard to get super bulled up when you have this level of old crop production.

The largest ever by a wide margin.

Although we should see a decline in production for new crop. Potentially a rather large one.

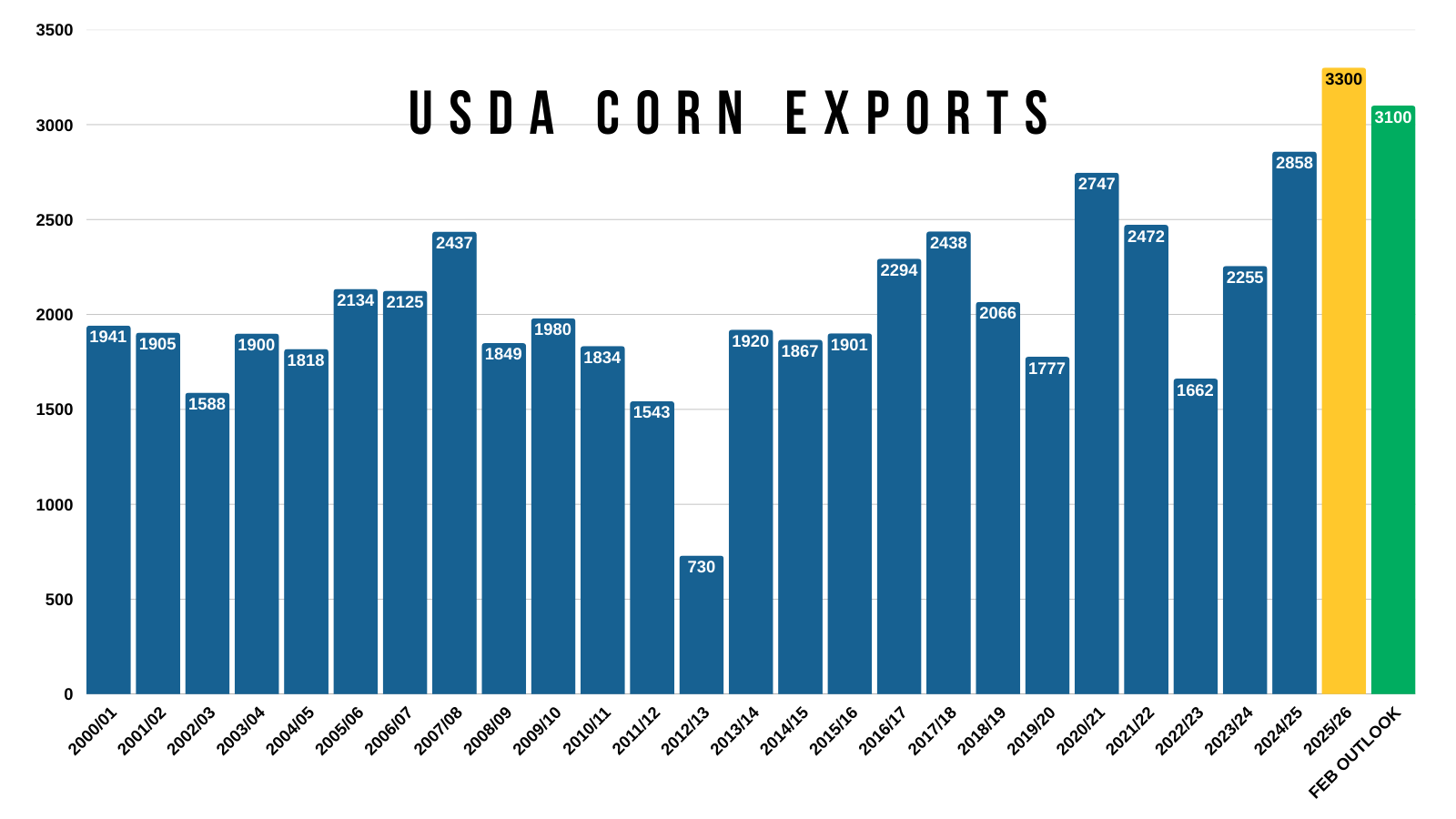

At the same time, demand is as great as it's ever been.

Just look at our export inspections vs other years.

This year is in a world of it's own.

Almost 50% better than the previous record at this point in the year.

So demand should prevent us from getting "too cheap" when looking forward.

The new crop story?

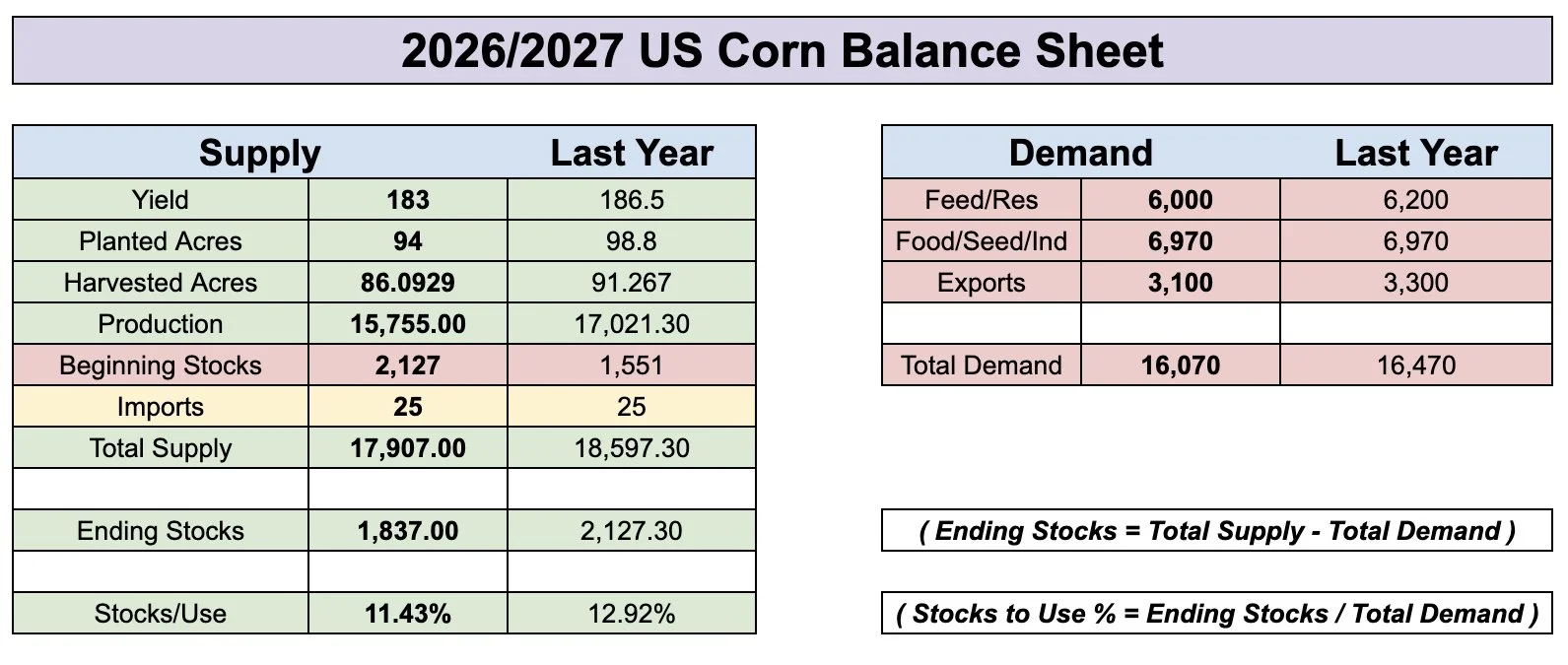

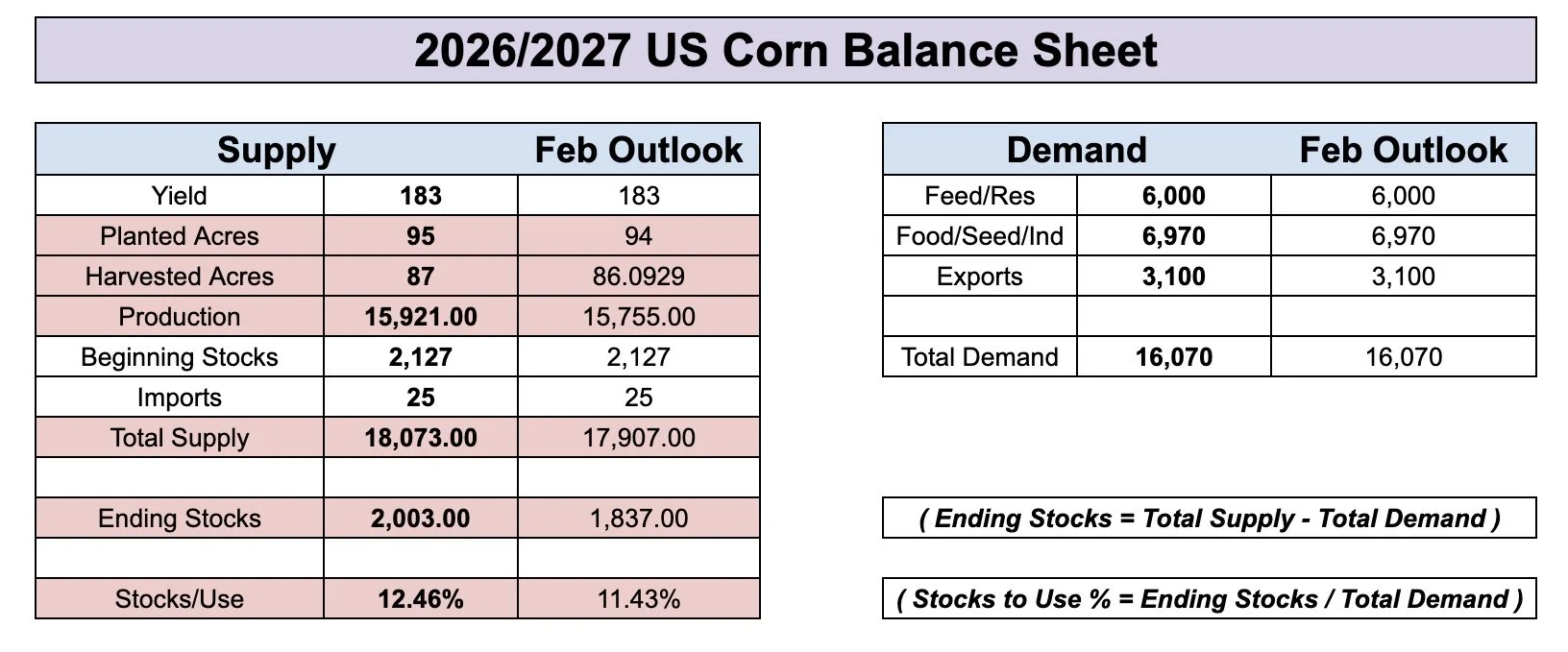

Here is the preliminary balance sheet from the USDA outlook.

I showed this Friday but wanted to dive into it a little further.

They have a 183 yield, 94 million acres, and a 1.84 billion bushel carryout.

It feels like acres could definitely be closer to 95, but if this is the balance sheet they actually use I view it as having friendly potential.

The USDA would be saying we need a 183 yield just for our carryout to be -300 million bushels lower than last year. With production being -1 billion less than last year.

This is with them expecting exports to be -200 million lighter than last year.

(Green = bullish vs last year) (Red = bearish vs last year)

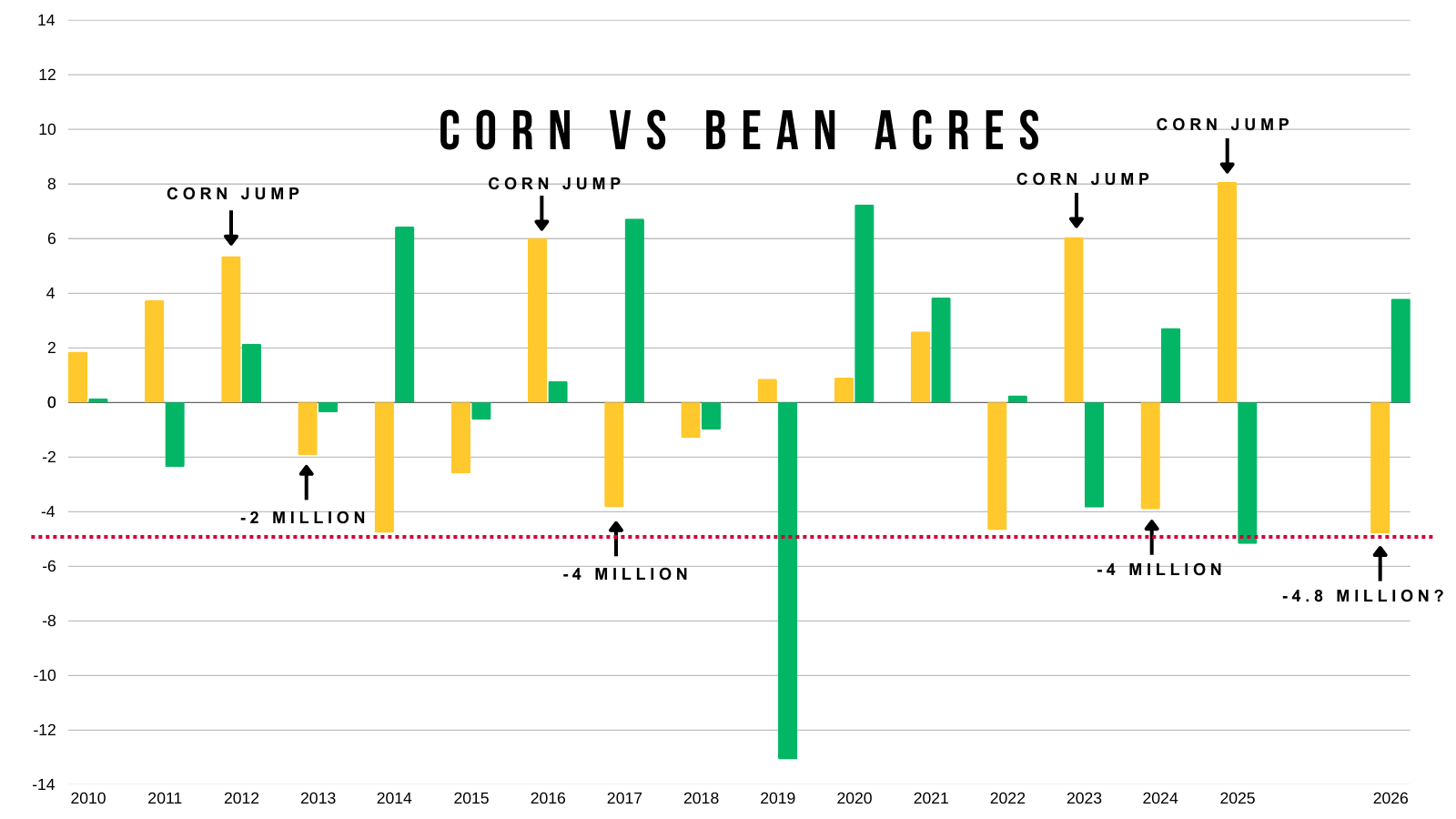

Here is why it feels like acres might not be as low as 94 million.

That would be one of the larger drops we've ever seen year over year.

Naturally when we see massive corn acres, we drop between 2-4 million the next year.

94 this year would be nearly a 5 million drop.

What if acres were 95 instead of 94?

If you took the USDA's balance sheet from the Feb outlook and simply bumped the acres by 1 million.

That alone would push the carryout right back to 2 billion bushels compared to the 1.84 billion the outlook has right now.

As it adds over +150 million bushels of supply.

So acres will be an important number.

Let's just say acres do wind up being 95 million.

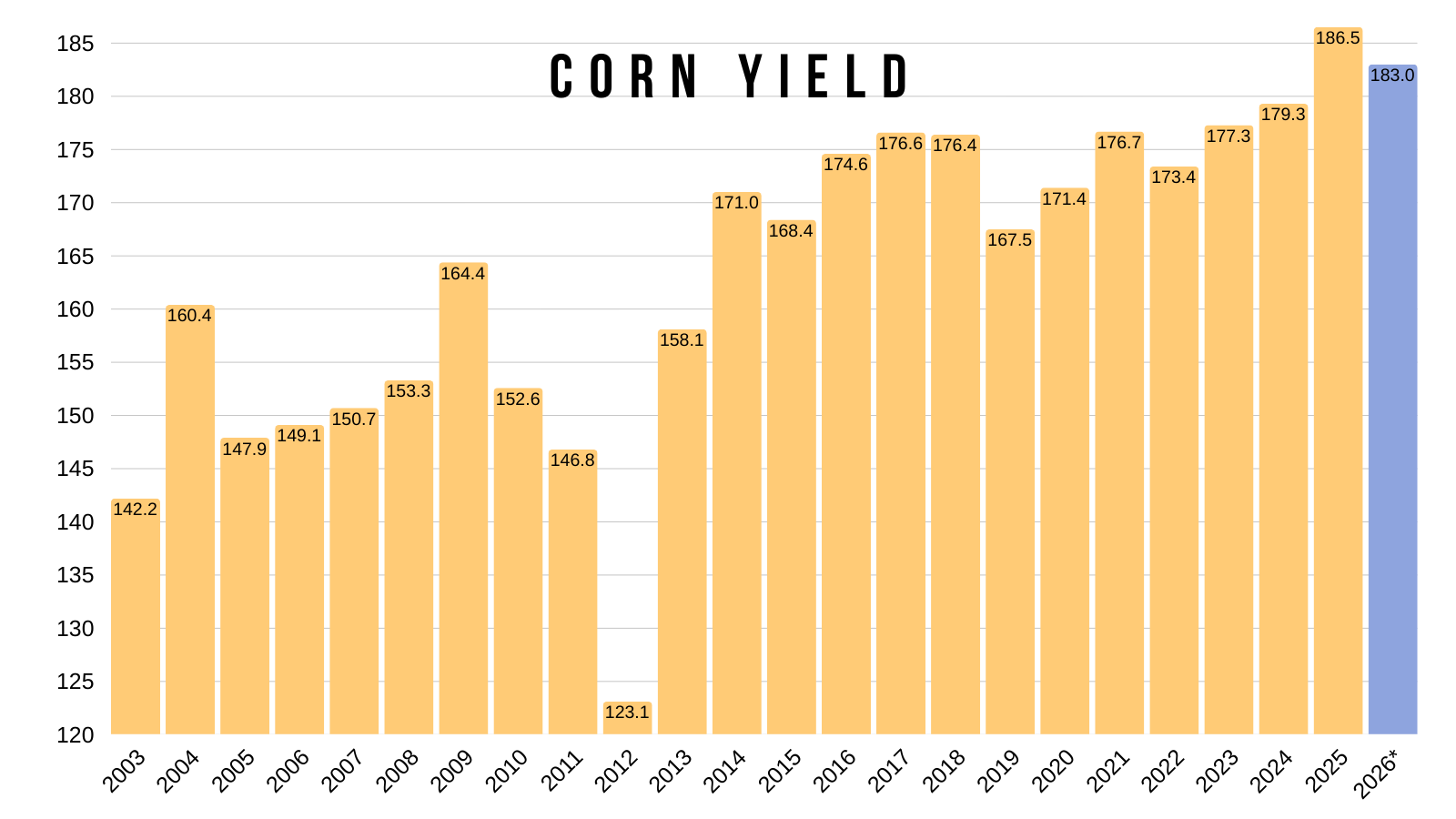

What happens if yield falls short?

We've seen a record 3 straight years in a row.

The longest record since the 80's.

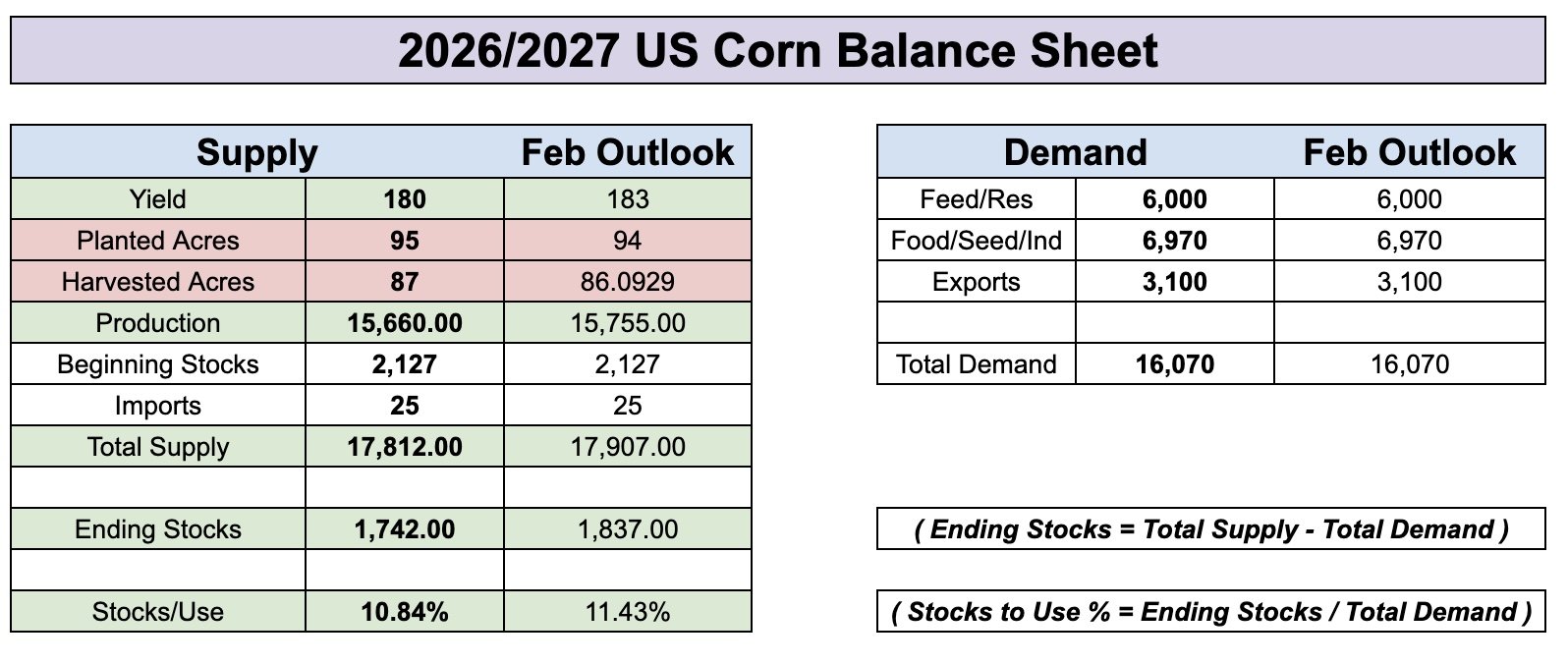

Here is the balance sheet with 95 million acres and a yield of 180.

It drops your carryout to around 1.75 billion and prints a 10.80% stocks to use ratio.

That wouldn’t be considered "bull market" bullish. But would not be a bearish figure.

It's way friendlier than the current 2.20 billion carryout we have right now for old crop.

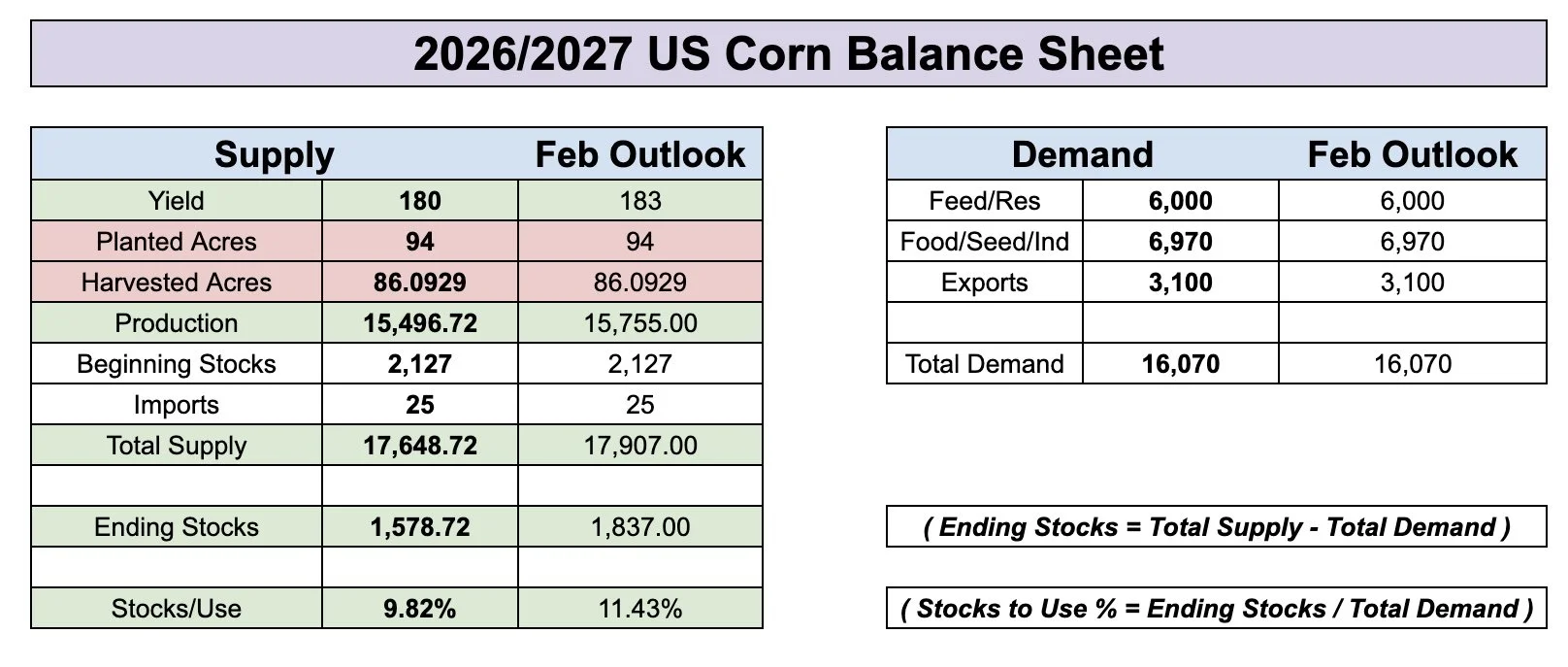

Here is what it looks like if you left the acres at 94 million and dropped yield to 180.

It prints a clear bullish scenario.

With a 1.58 carryout and a sub 10% stocks to use ratio.

The demand numbers will of course change, but you get the idea.

The US will still need a large yield to keep the new crop balance sheet as large as it is for old crop.

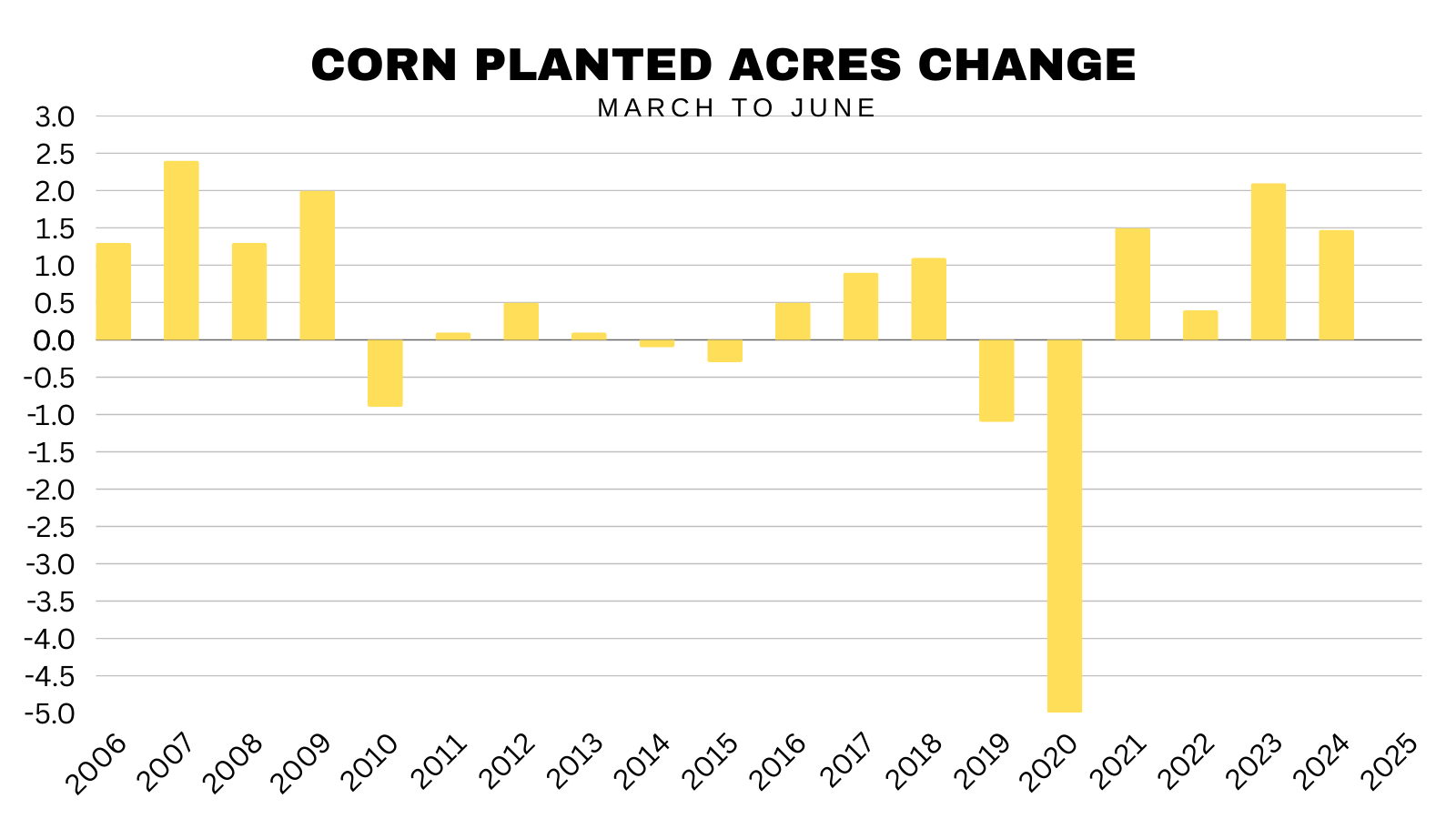

There is a world where the USDA keeps the acres at 94 million for now, but then bumps them in the June report.

The USDA has a tendency to raise the acres from the March intentions to the June report.

They've raised acres the last 7 of 10 years in June.

This is another reason why we can seasonally top around that June report.

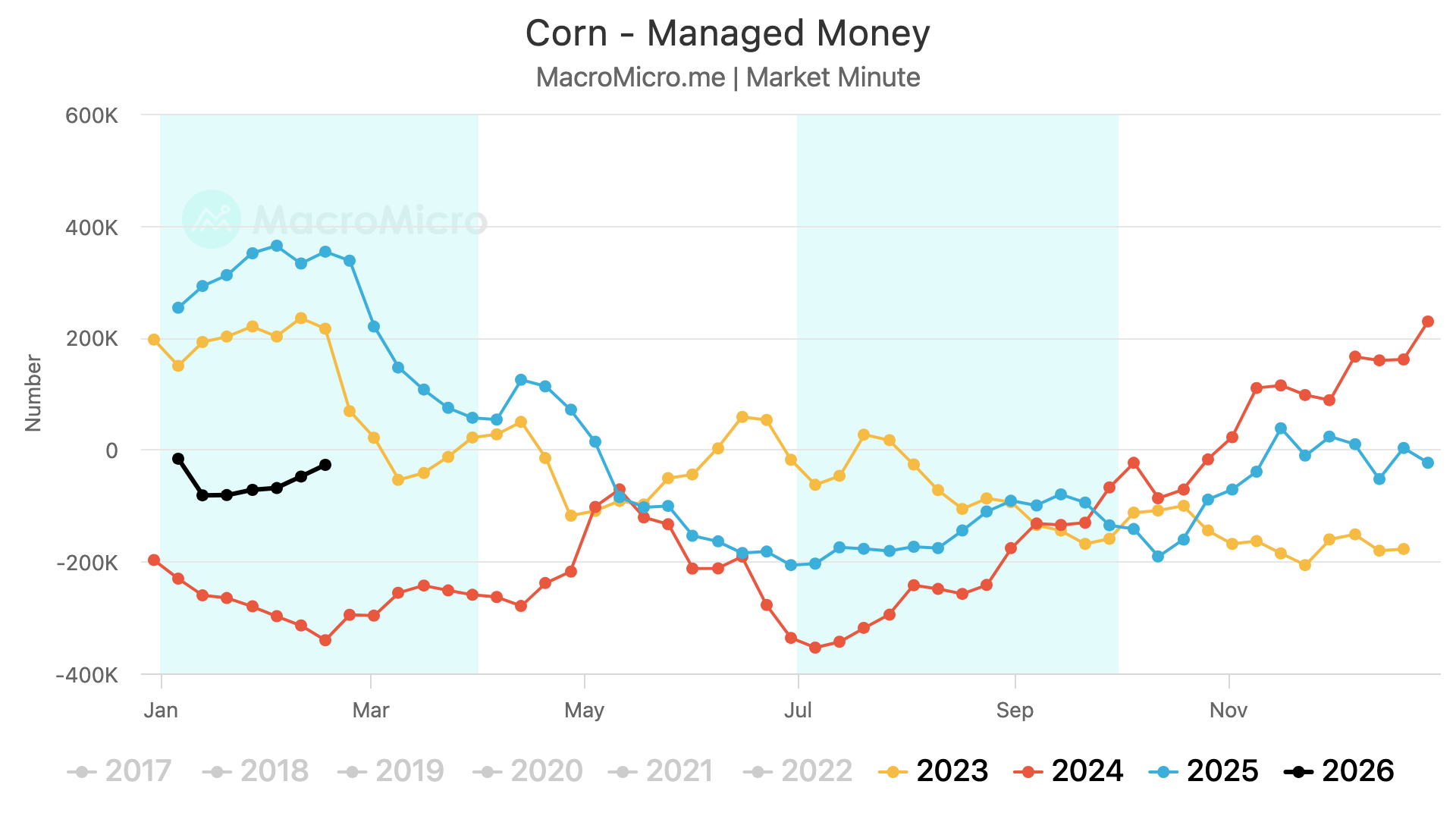

The funds:

They are currently slightly short on the corn market, but pretty much neutral.

Last year around right now, they were crazy long.

So it doesn’t feel like we have this massive amount of downside risk like we saw last year, where we fell -$1.20 from Feb to July.

As I don’t see a reason for them to now suddenly flip mega bearish out of nowhere ahead of all of the uncertainties the planting and growing season brings.

Technicals:

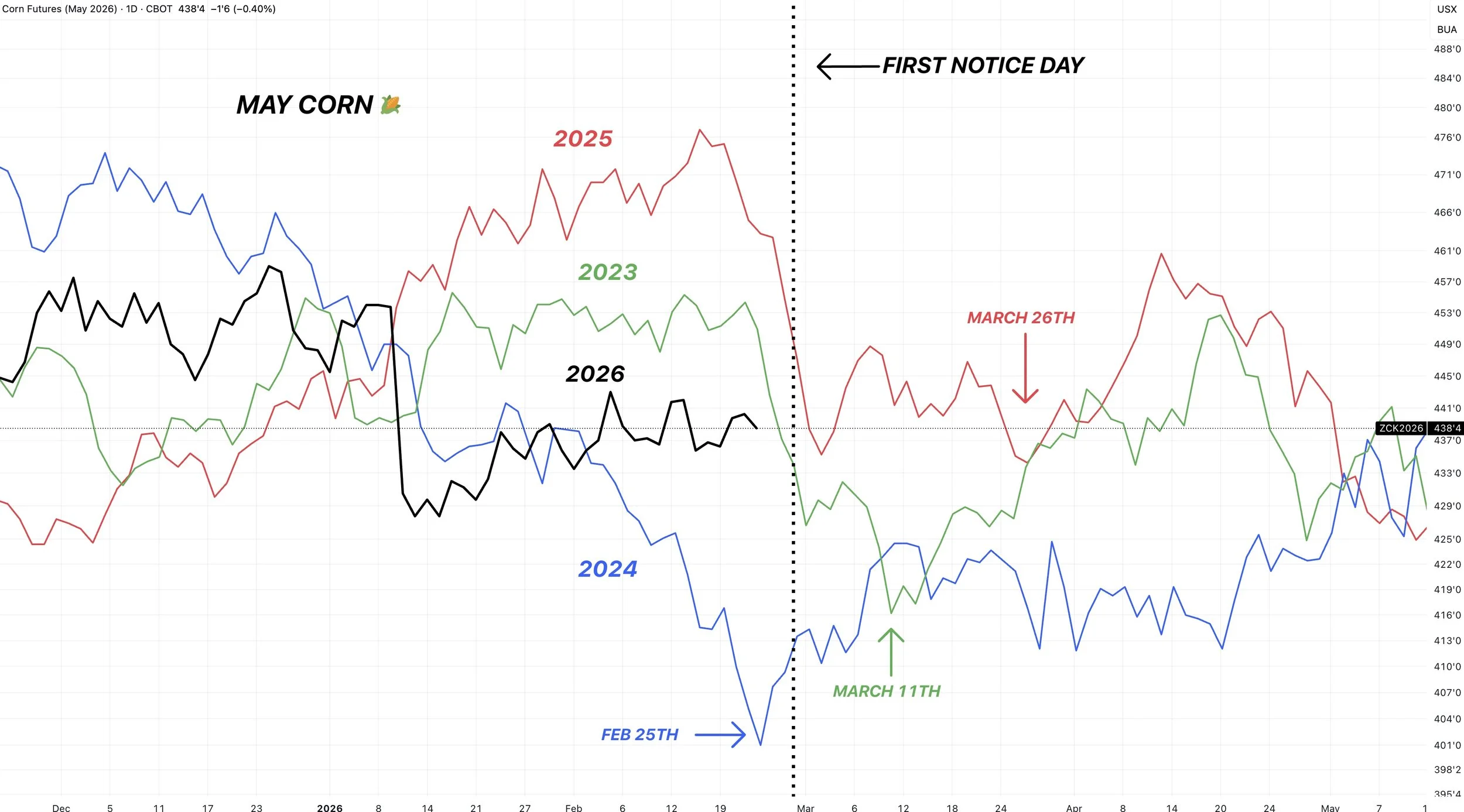

May Corn:

Still range bound here.

Failing at the old support level from last year.

Need to break back into that old range to open the door to further upside.

We still have a potential bear flag to aware of.

We need to hold $4.33 to keep an upward bias. Fail to hold that and we could go and test the lows.

That is the 61.8% retracement to the lows.

Soybeans

Fundamentals:

Despite all of the tariff headlines, it appears Trump is still scheduled to meet with China in April.

I gave my reasoning Friday and why I don’t think the Supreme Court tariff ruling with have a major immediate impact on grains.

Some argue that China has no reason to buy soybeans now because Trump lost his leverage.

Tariffs aren’t going anywhere in my opinion.

China still has tariffs on them. Their effective tariff rate is 24% now, compared to 32% before the court decision.

However, for soybeans to go and take out those November highs we are probably going to need to see some confirmation of China buying.

It really is that simple. If China starts to buy like Trump said they "might" we can go higher.

If they do not buy, we will probably head lower. As this entire rally has been based on the thought of them buying.

We have still received no confirmation of them buying.

That meeting with China in April is still a long ways away, so that does add some risk here. That the market might get tired of the story if China doesn’t buy until then.

You have some people arguing that Brazil's harvest is the slowest it's been since 2020.

I don’t think that really matters, as the crop is by far way larger than it was back then.

They are still going to have a record crop that is about to hit the export market right now.

Some argue that Brazil's crop is $1.25 cheaper than ours, so China might cancel what they've bought from us to buy Brazil's instead.

However, China is very aware of Brazil's crop.

I think if that was the case, they would have already done it by now.

But in the short term, I do see some risk in this market if China doesn’t start to step up soon.

The market has been holding on to China optimism as well as bio fuel optimism. But eventually it will probably want some results.

Soybean acres are going to be up this year, and Brazil's record crop is hitting the market.

We still have potential moving forward, but I do like rewarding this market if you have not yet done so.

As a pullback wouldn’t surprise me at all, we could very well be due for one. After this sideways trade, it feels like the market is ready to make a move.

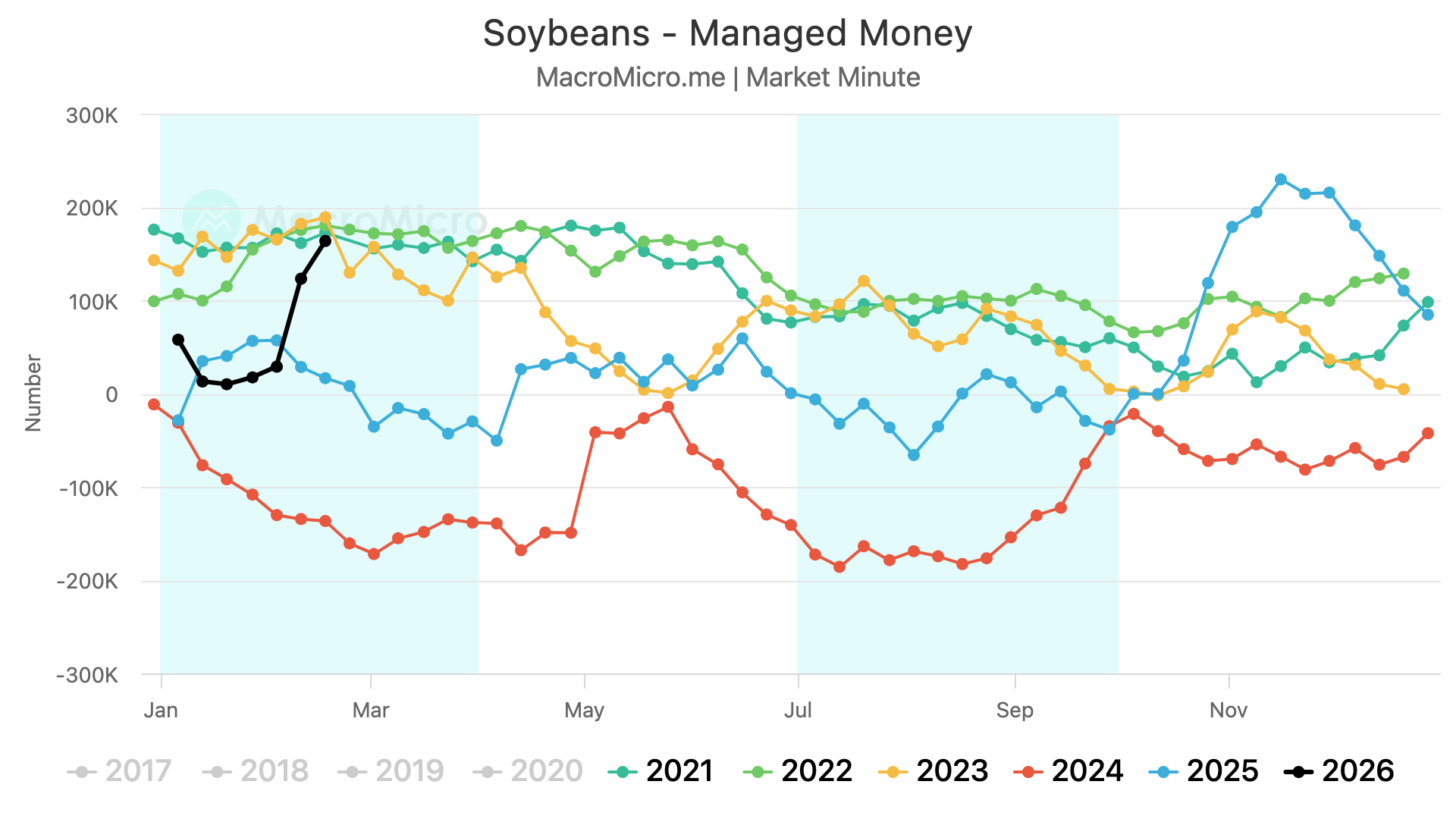

The funds:

The funds are back and are super long soybeans again.

On par with how long they were during the bull market.

This is about as long as they have ever been for this time of the year.

However, you have to keep in mind that nothing has actually changed on the balance sheets over the last several months.

The market is going higher on what Trump has said China will do. So the funds will need to see that happen eventually.

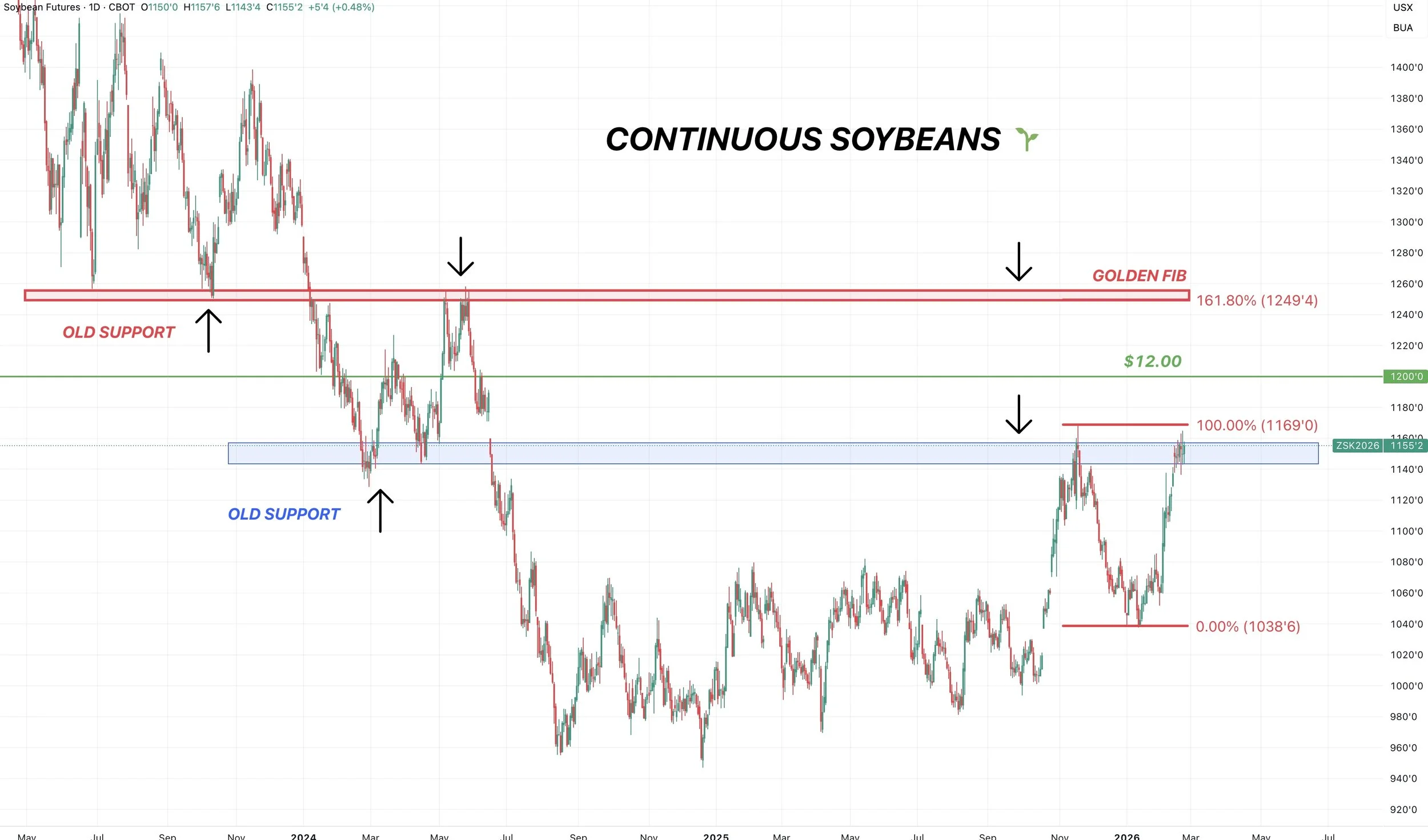

Double Top?

Here is a reason to have some caution up here.

This is the continuous chart.

We are right up against those November highs.

We've been trading sideways, struggling to break above them.

Volume has also been declining on this rally.

Break above this level, and the door higher is wide open, but we have been struggling here.

Big Picture Chart:

Still sitting right at a pretty big resistance level.

This was the Nov highs.

It was support from 2024 twice.

Struggling here makes sense.

Since it's resistance, we want to reward this level in some menner.

If we can clear this level, the next spot to reward is $12.

After that, $12.50 is the next level. It was our 2024 highs. It was our 2023 lows.

Wheat

Long term trend change?

I showed this last week.

The week market is currently having it's longest sustained rally since 2021.

This makes me think we might be seeing a long term shift in the trend.

But that doesn’t mean we shouldn’t take advantage of the rally.

We alerted a sell signal last week as we were approaching our targets.

Link to Sell Signal: Click Here

Long term, I think the wheat market has potential.

But short term, you can’t forget that the world isn’t running out of wheat.

Globally there just isn’t major issues in the world, so it makes sense that this rally is losing some steam without a driving factor.

The US situation is still the most bearish it's been in a while.

But at a certain point, when everything is bearish, the only way to go is a less bearish situation long term. As at a certain point, the most bearish things will be priced in.

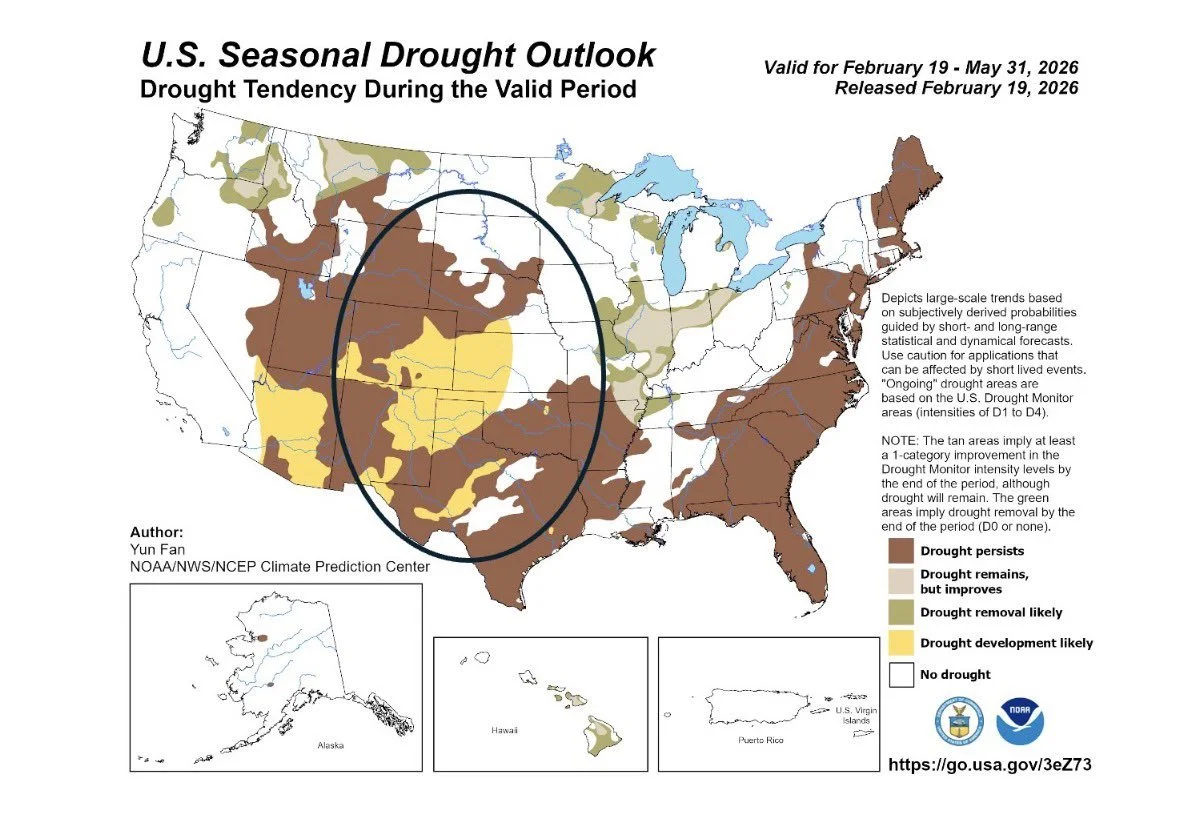

Drought?

It is awfully dry in the southern plains.

This is maybe a slight part of the reason for the recent strength.

However, the market probably won’t take major notice until the crop starts to wake up in April.

If it stays dry, though, definitely something to keep on your radar.

March & April Weakness?

I showed the data behind this on Friday.

March and April is seasonally a weak time period for wheat.

From last Friday until mid-April the wheat market has traded lower 15 of the last 20 years.

If you look at the seasonal chart, a pullback here would be right on cue.

Weekly KC:

This was another reason for the sell signal last week.

We rejected right at those highs from June on the front month contract chart.

Finding some resistance here makes sense.

Long term, this is still a solid looking chart. But a pullback after this breakout should not be a surprise.

Here is a zoomed in view.

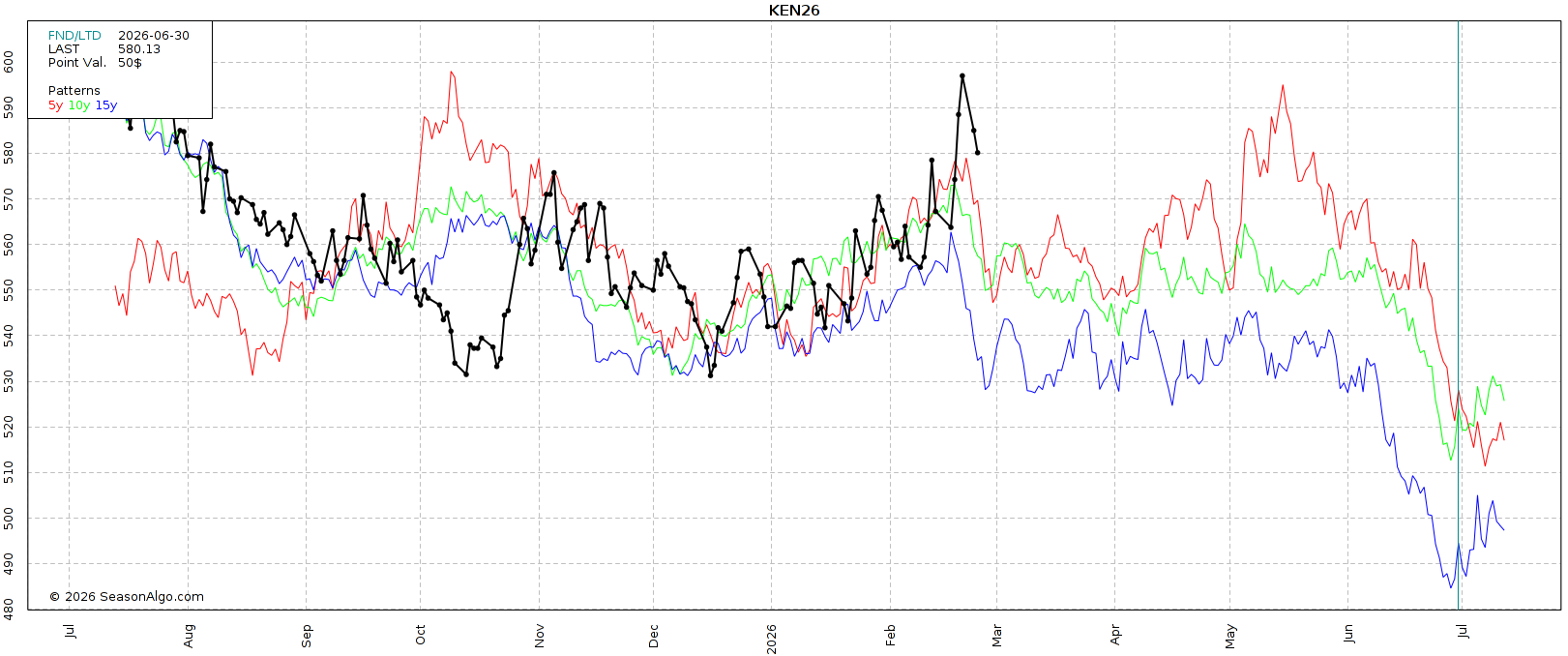

May KC:

We hit that upside target. The golden zone up to the June highs.

We are already -24 cents off of Friday's highs.

The rally is finding resistance here as expected.

It would make sense for us to now come down and test that point of breakout.

Trying to turn that old resistance into some new support.

May Chicago:

Chicago also tagged that target box.

We clawed back 50% of the June highs.

This same level is old support.

Struggling here wouldn’t be a surprise.

Cup and Handle?

We could potentially be setting up for a cup and handle pattern in Chicago wheat.

It's a friendly pattern but could take some time to play out.

We have the cup that took 5 months.

We could now get the handle, where we struggle for a little while before eventually going higher.

Cattle

Cattle is dealing with a few headlines.

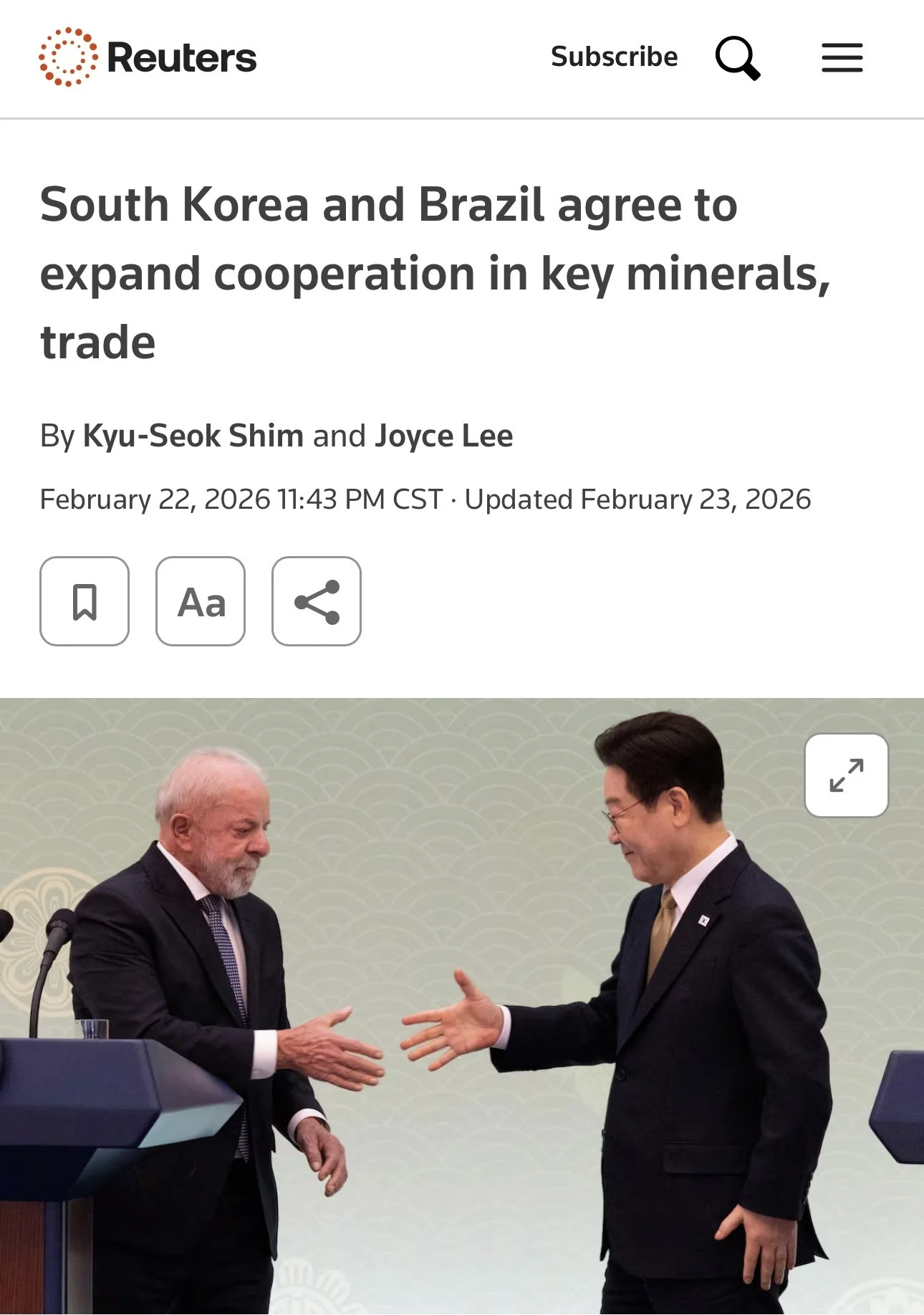

South Korea & Brazil Deal:

We have talk that South Korea and Brazil are making a trade deal. Which would in theory lead to less demand for US beef.

It's an issue because South Korea is the #1 buyer of US beef. It's not something that is going to make a big impact right away, as it will take a while for it to play out. But it's a headline risk and long-term factor.

Plant Strike:

Wholesale boxed beef spiked today because the market is nervous a major packing plant might shut down.

It sounds like workers at at the JBS Greeley, Colorado plant might go on strike. As the workers have done some preparation and have threatened to do so.

This is one of the biggest plants in the US.

A plant shutdown is usually bearish for cattle futures but bullish for boxed beef.

If they shut down, it would create a supply back log. The cattle at Greeley have nowhere to go.

With one less big buyer in the market, the other packers have more leverage. So they won’t have to bid as aggressively. Which can be negative for cash.

Overall I still see headline risk in this market. Not to mention screwworm along with the border.

Technicals:

April Feeders

Volume has switched to April feeders.

This chart still feels top-heavy in my opinion.

We have about as clear of bearish divergence as you can get. The RSI is fading lower while prices have grinded higher.

Bulls want to see us hold that first support box.

If we fail there, it could open the door quiet a big lower towards the golden zone of the entire rally.

April Live

Similar set up.

Clear bearish divergence still makes me pretty cautious.

Failure to hold the first support level could spark a real correction.

Past Sell or Protection Signals

Feb 19th: 🌾

KC wheat sell signal & hedge alert.

Feb 6th: 🌽 🌱

Corn & soybean sell signal & hedge alert.

Feb 4th: 🌱

Soybean sell signal & hedge alert.

Dec 11th: 🐮

Cattle sell signal & hedge alert.

Dec 5th: 🐮

Cattle sell signal & hedge alert.

Nov 17th: 🌱

Soybean sell signal & hedge alert.

Nov 13th: 🌽 🌱

Managing risk in corn & beans ahead of USDA report.

Oct 28th: 🌽

Corn sell signal & hedge alert.

Oct 27th: 🌱

Soybean sell signal & hedge alert.

Oct 13th: 🐮

Cattle sell signal & hedge alert.

Aug 22nd: 🌱

Soybean sell signal & hedge alert.

July 31st: 🐮

Cattle sell signal & hedge alert.

July 10th: 🐮

Cattle sell signal & hedge alert.

CLICK HERE TO VIEW

June 5th: 🐮

Cattle sell signal & hedge alert.

June 2nd: 🌾

MPLS wheat sell signal.

April 10th: 🌽

Old crop corn sell signal.

March 19th: 🐮

Cattle hedge & sell signal.

Feb 18th: 🌽 🌾

Old crop KC wheat & old crop corn signal.

Jan 23rd: 🌽 🌱

Corn & beans old crop sell signal.

CLICK HERE TO VIEW

Jan 15th: 🌽 🌱

Corn & beans hedge alert/sell signal.

Jan 2nd: 🐮

Cattle hedge alert at new all-time highs & target.

Dec 11th: 🌽

Corn sell signal at $4.51 200-day MA

CLICK HERE TO VIEW

Oct 2nd: 🌾

Wheat sell signal at $6.12 target

Sep 30th: 🌽

Corn protection signal at $4.23-26

Sep 27th: 🌱

Soybean sell & protection signal at $10.65

Sep 13th: 🌾

Wheat sell signal at $5.98

May 22nd: 🌾

Wheat sell signal when wheat traded +$7.00

Want to Talk?

Our phones are open 24/7 for you guys if you ever need anything or want to discuss your operation.

Hedge Account

Interested in a hedge account? Use the link below to set up an account or shoot Jeremey a call at (605)295-3100.